Japan Markets ViewYear-End Market Complexity Seasonal NT Ratio and Long-Term Shifts to Watch

Apr 04, 2025

[Keiichi Nakayama, QUICK Market Eyes] March 27 is the last trading day before the ex-rights date for companies whose fiscal year ends in March, etc. From that day through March 28, institutional investors tend to “reinvest dividends” by investing in advance future dividend payments to be received. This is a complicated time of supply- demand structure, with the NT ratio, which is the Nikkei 225 divided by the TOPIX, likely to decline seasonally and fewer share buybacks toward the end of the fiscal year. The Japanese stock market may enter a correction phase through the start of the new fiscal year. However, we would like to keep an eye market changes and the supply-demand structure from a long-term perspective.

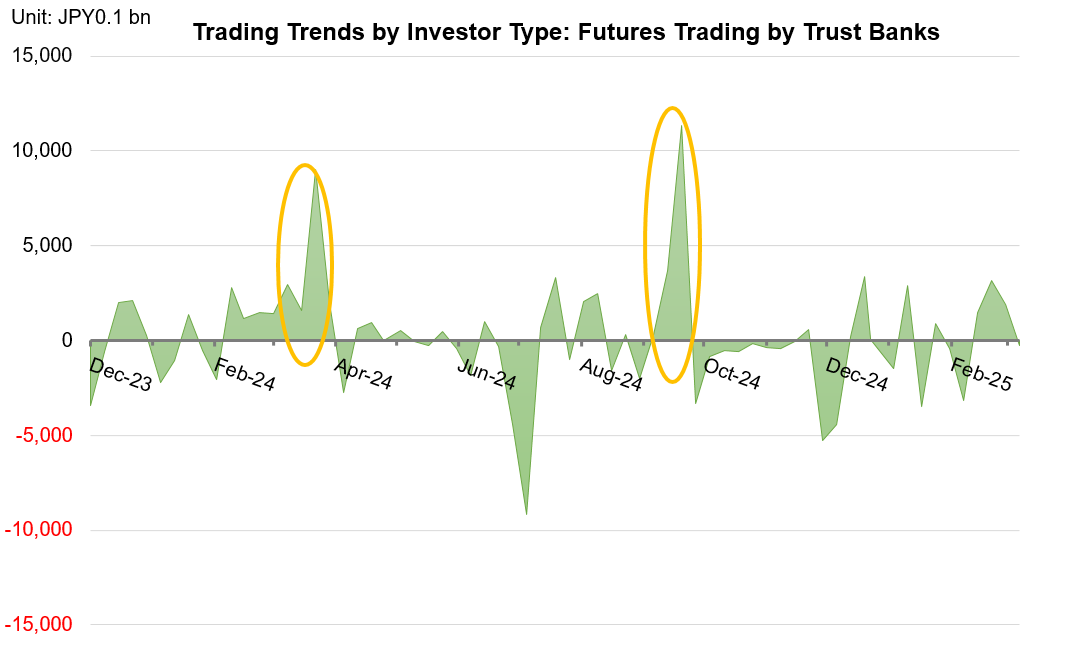

Timing of NT Ratio Decline with Dividend Reinvestment of JPY1.4 Tn

Dividend reinvestment regularly serves as a factor affecting end-of-year supply-demand balance. It is a practice by institutional investors who invest in index-linked assets to avoid tracking errors, the deviation between the investment index and investment performance until they actually receive dividends. Takehiko Masuzawa, trading head at Phillip Securities Japan, estimates that buying demand will amount to JPY1.4 tn, including JPY250 bn for assets linked to the Nikkei 225 and about JPY1.15 tn for those linked to the Tokyo Stock Price Index (TOPIX).

The trading trends by investor type published by the Japan Exchange Group (JPX) indicate dividend reinvestment taking place in the market. Trust banks tend to be net buyers of futures in the last weeks of March and September. In particular, they purchase more TOPIX futures than Nikkei 225 futures, tracing the estimated data based on dividend reinvestment.

*Compiled based on the JPX and QUICK data.

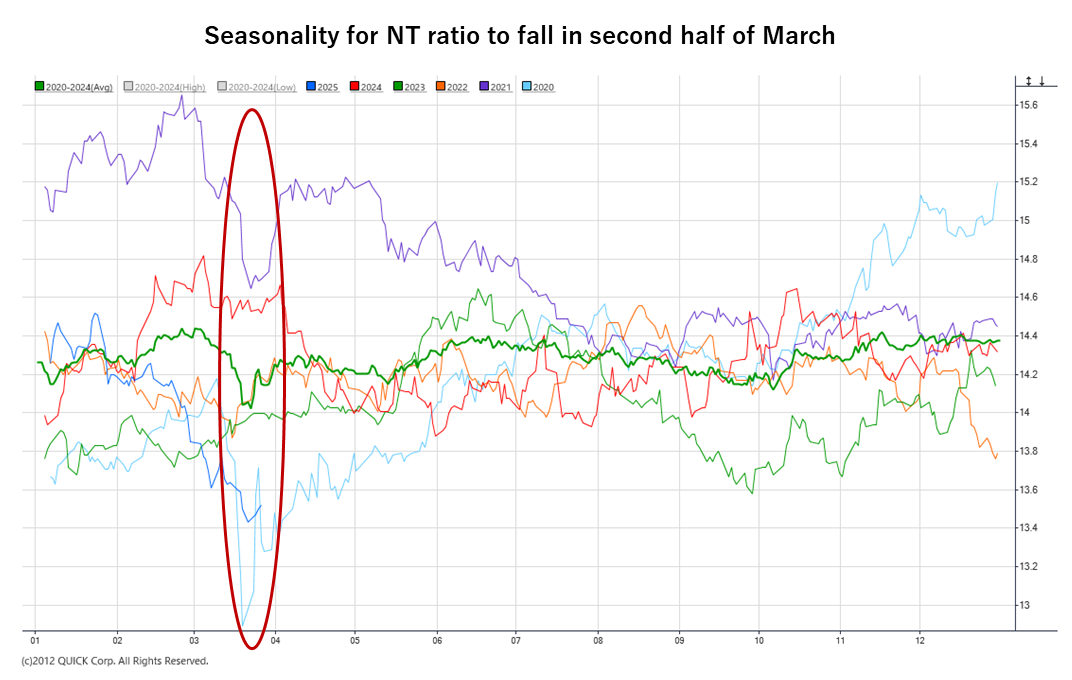

The NT ratio shows seasonality also influenced by the vigorous dividend reinvestment trend. The ratio temporarily dropped to 13.41 on March 21, the lowest level since April 6, 2020, due in part to significant gains in banking stocks on expectations of the BOJ’s monetary policy normalization.

*Created from the QUICK chart function.

Further Forward Dividend Reinvestment, Reduced Share Buybacks, and Profit-taking Selling May Weigh on the Near-Term Market

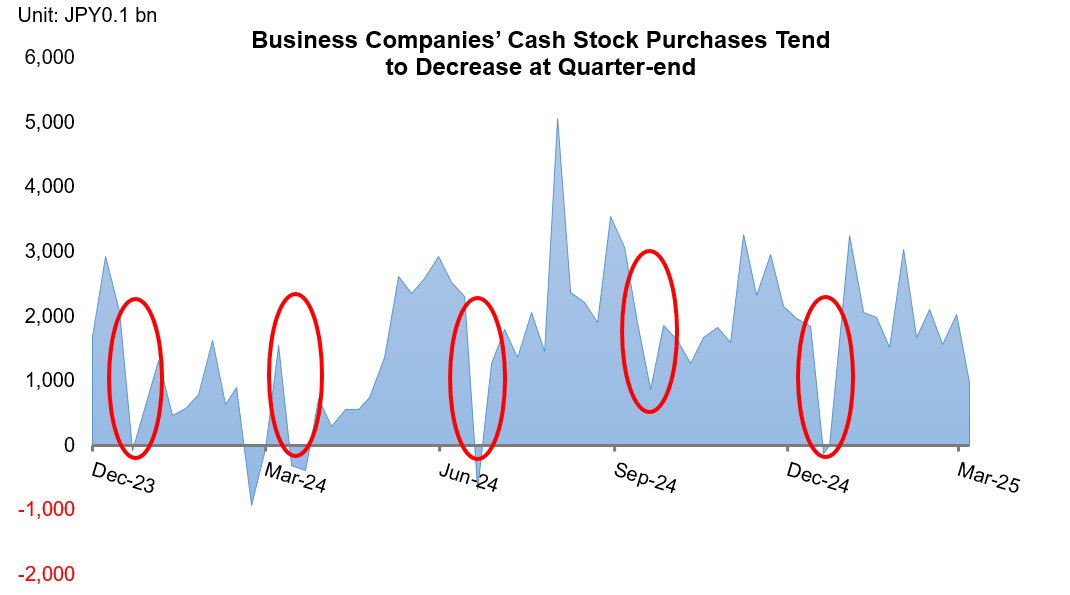

Seiichi Suzuki, chief equity market analyst at Tokai Tokyo Intelligence Laboratory, noted, “Dividend reinvestment at the end of March and September is a regular event. Further forward buying of TOPIX-linked stocks led to the decline in the NT ratio.” At the end of the quarter, companies tend to refrain from share buybacks. In addition, “investors’ aggressive profit-taking selling due to rising market prices and ‘selling shares to post profits’ by Japanese companies in April may put Japanese stocks in a correction phase and a temporary reversal of the NT ratio,” according to Mr. Suzuki.

*Compiled based on the JPX and QUICK data.

However, Mr. Suzuki sees the correction phase as a new “planting opportunity” in light of long-term supply-demand balance and market changes. He believes that listed companies will continue to increase dividends to shareholders for the purpose of returning the retained earnings they have accumulated over the years to shareholders, and that high levels of share buybacks will continue. He views the long-term supply-demand balance and structural changes in the market, such as the increased inflow of activist investors into the Japanese market and changes in corporate behavior, will continue to underpin the Japanese stock market.

Governance Reform Making Progress in Japan

In a report dated March 19, Nozomi Moriya, strategist at UBS Securities, noted, “Governance reform in Japan is making progress with multiple drivers.” According to Ms. Moriya, the progress was confirmed through the Japanese government and the Tokyo Stock Exchange’s commitment to reform at the ICGN 30th Anniversary Conference – Asia, held on March 4-5 by organizations, including the International Corporate Governance Network (ICGN); and also by progress in engagement by institutional investors in Japan as well as activist investors.

Ms. Moriya also sees corporate activity, not as a formal change, but as an ongoing substantive change in expanding corporate value creation efforts. As a result, she says, Japanese companies’ return on equity (ROE) could increase. Some market strategists argue that there are no new themes in Japan. However, it is necessary to watch for the supply-demand structure and changes in companies that require a long-term perspective.

(Reported on March 26)

Related dataset : Share Buybacks Data

Discover datasets unique to the Japanese equity market : Visit QUICK Data Factory

Shift from Popular Stocks: Unwinding Begins

Share Buybacks Resolved in April Exceeds JPY3.5 Tn, Continuing to Support Supply-Demand Balance

Follow us on LinkedIn to stay updated with Japan Markets.