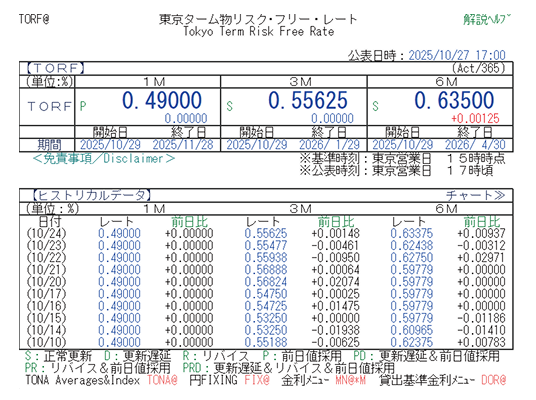

TORF(Tokyo Term Risk Free Rate)

Japanese Yen Term Risk Free Rate Designated as a “Specified Financial Benchmark”

TORF is a “Specified Financial Benchmark” as defined by the Financial Instruments and Exchange Act. It is a term risk free rate (interest rate on risk free assets) calculated and published daily by QUICK Benchmarks Inc. (QBS), which is designated as a Specified Financial Benchmark Administrator. It is one of the successor benchmarks to the London Interbank Offered Rate (LIBOR), whose publication ceased at the end of 2021.

- Features and Outline of TORF

- TORF Adoption and Market Acceptance Status

- How to Access TORF

- Information Regarding the Use of TORF

Features and Outline of TORF

Features

- Term interest rate based on the “risk free rate” of Japanese yen

- Adopts the “fixing in advance” method, where the applied interest rate is fixed at the beginning of the period.

- Interest rate reference period and calculation period are the same.

Outline

| Official Name | Tokyo Term Risk Free Rate | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Abbreviation | TORF | ||||||||

| Linkage with the Market |

|

||||||||

| Interest Rate Determination Method | Adopts the “fixing in advance” method, where the applied interest rate is fixed at the commencement of the interest period. | ||||||||

| Uses | Reference rate for commercial transactions, including loans and bond issuances, asset valuation. | ||||||||

| Advantages of Using TORF | Like Japanese yen LIBOR, it allows borrowing and lending rates to be set in advance, enabling smooth management and operation using conventional systems. | ||||||||

| Data Provided |

Calculation Time: 3:00 pm JST on a Tokyo business day |

||||||||

| Source Data for Calculation |

|

||||||||

| Calculation Methodology | It is calculated from data on derivative transactions (OIS) based on the uncollateralized overnight call rate (Tokyo Overnight Average Rate: TONA), which involves almost no credit risk of financial institutions. The Waterfall methodology is adopted, whereby executed transaction data is used first. If there is no applicable data, the next level of data is used. Details of the calculation methodology can be downloaded below. |

TORF Adoption and Market Acceptance Status

TORF is a relatively new interest rate benchmark, and its adoption rate is gradually increasing.

| Financial Institutions Response |

|

|---|---|

| Corporations Response |

|

| Current Market Penetration |

|

How to Access TORF

Accessing TORF via QUICK Services

Subscription to one of the following services is required:

| Target Services | Qr1, QUICK Workstation, QUICK Workstation Astra Manager Package, QUICK Asset Design PRO, QUICK APIs, QUICK Feed, and others. | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| For Inquiries |

※QUICK Money World (24H Delayed): https://moneyworld.jp/page/torf.html |

|||||||||

| For Inquiries |

Quote Code

※QUICK Money World (24H Delayed): https://moneyworld.jp/page/torf.html |

Other Publication Sources

- The Nikkei (Morning Edition)

- Nikkei NEEDS service

- Refinitiv(Tile:<JPYTRR=QCKJ>、RIC Code:<JPYTRR1M=QCKJ>、<JPYTRR3M=QCKJ>、<JPYTRR6M=QCKJ>)

- Bloomberg(TORF<Go>)

Information Regarding the Use of TORF

License Agreement

A license agreement with QUICK is required to use TORF. Please refer to the “Agreement Sample (PDF)” and the“User License Price List(PDF),” then contact us below.

※Please refer to the “Application Form Sample (PDF)” for instructions on how to complete the application form.

※For details regarding the TORF license, please also see the“TORF License Guide (PDF)”.

Redistribution License

To redistribute TORF, a license agreement with QUICK is also required. Please refer to the “Redistribution License Price List (PDF),” then apply using the contact form.

Other Related Documents

Please also confirm the content of the documents on the following QUICK Benchmarks Inc. (QBS) website.