Japan Markets ViewPPIH (7532) Aims for JPY4 tn in Sales through Its New Business Format, “Robin Hood”

Apr 10, 2026

[Akira Motoyoshi, QUICK Market Eyes] Pan Pacific International Holdings (PPIH), operator of the Don Quijote discount store chain, continues to see its business grow. Since its founding in 1989, PPIH has achieved 36 consecutive years of growth in both revenue and profits. It has grown into a massive retail group with consolidated sales exceeding JPY2 tn. Its newly launched retail format, “Robin Hood,” is expected to drive further growth and is worth watching.

The company’s greatest strength lies not simply in offering low prices, but in having built a “unique ecosystem” in which its corporate culture and business model are fully integrated. PPIH believes that its business concept of “CV (Convenience) + D (Discount) + A (Amusement)” creates added value where “1+1=∞ (infinity).” Furthermore, the company has consistently adhered to a “store-based management” approach since its founding, empowering each store with a high degree of autonomy over product procurement, pricing, and merchandising. This model enables immediate responses to the needs of local communities and trade areas, resulting in strong consumer support.

Despite competing with general merchandise stores, drugstores, and discount stores, it overwhelms its competitors in capturing spending by foreign visitors to Japan. This is not simply due to the large number of stores; rather, the company has established a unique brand position (tourist-oriented retail) that has led people to say, “I visit Japan because Don Quijote is there.” Its amusement factor, which prevents it from being drawn solely into price competition, is the primary differentiator. In addition, the sales ratio of Don Quijote’s private label brand, such as “JONETZ,” and original equipment manufacturer (OEM) products is steadily growing. Product development that accurately captures customer needs and the strategy of converting staple items to OEM have been successful. These factors contribute significantly to improving the gross profit margin.

In the long-term business plan “Double Impact 2035” announced in August 2025, PPIH set targets for the fiscal year ending June 2035, including net sales of JPY4.2 tn and operating income of JPY330 bn (actual results for the fiscal year ending June 2025: JPY2.2467 tn in net sales and JPY162.2 bn in operating income). The company aims to capture the vast opportunities primarily latent in the Japanese market. Its core business, “Don Quijote – Astonishingly Affordable Store,” has shown unmatched strength in the inbound tourism market and large trading areas for weekend bulk shopping. However, the company historically struggled to capture the massive market of “everyday weekday shopping” within local neighborhood trade areas. To address this, the company launched a new food-focused format called “Robin Hood – Astonishingly Fun Store.” Robin Hood accurately captures the modern demand for affordability and time efficiency, focusing on four themes: “Low price, Great value, Fast, and Easy.” Under the concept of “More hassle-free than a supermarket and as fun as Donki (Don Quijote),” the company aims to seize the enormous opportunity to maximize customer Lifetime Value by establishing a complementary relationship between “Don Quijote” and “Robin Hood” tailored to customers’ lifestyles and circumstances. In general supermarkets, non-food products account for only about 10% of sales and floor space. In contrast, “Robin Hood” sets its non-food floor space at approximately 40% and its sales ratio at approximately 25%. By generating solid profits from high-margin non-food items and setting prices for fresh food and other goods at deeply discounted levels, the company aims to establish a robust profit base that competitors cannot replicate structurally.

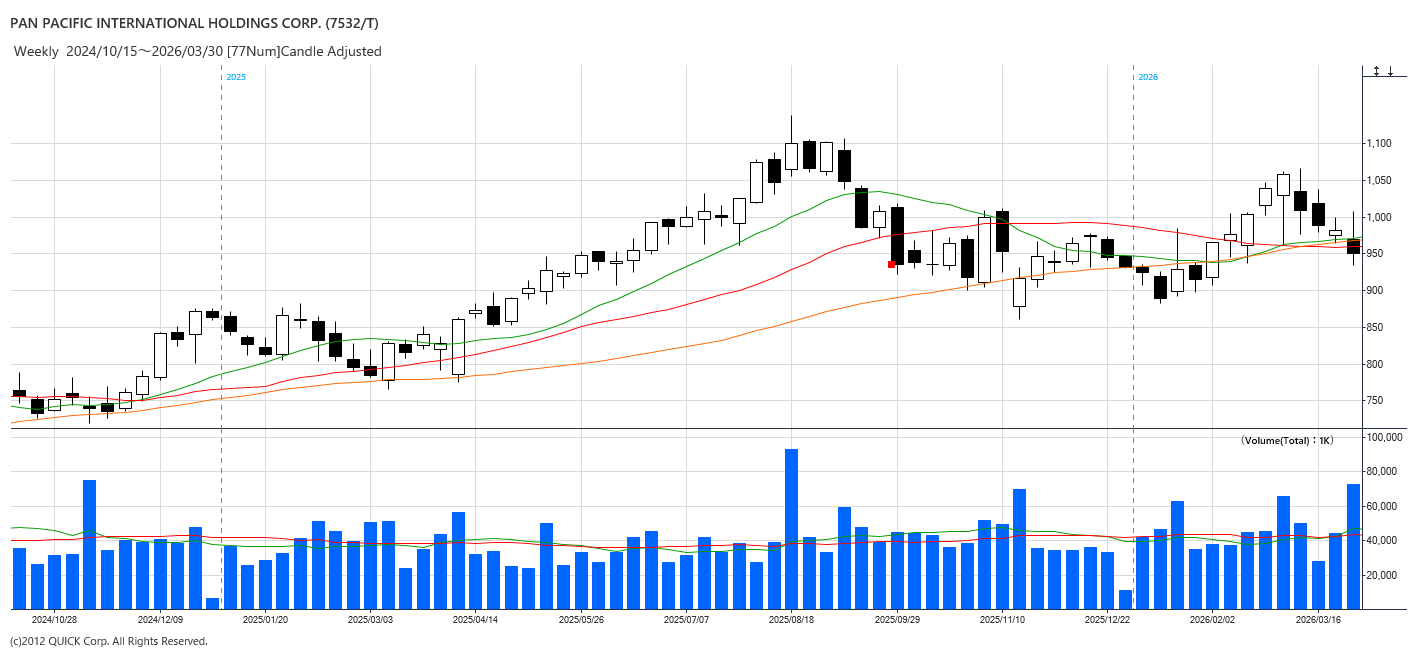

“Robin Hood” aims to capture “food demand in small trade areas” by leveraging a unique business model, which delivers both strong customer attraction and high profitability. The model is created by combining the “fresh produce procurement capabilities (traffic-generating power)” honed over approximately 20 years through past acquisitions—Nagasakiya in 2007 and UNY in 2019—with Don Quijote’s “merchandising capabilities (high profitability from non-food items).” Starting with five store openings in the fiscal year ending June 2026, the company plans to expand to 200–300 stores by 2035 with projected net sales of JPY600 bn and operating income of JPY36 bn. PPIH plans to expand its network through conversions of existing supermarkets and acquisitions, along with new store openings. The first major step is the acquisition of Olympic Group (8289), which operates a mid-sized supermarket chain. Olympic Group operates approximately 120 stores, primarily in the Tokyo metropolitan area. PPIH is expected to convert these stores to the “Robin Hood” outlets following the acquisition. This move aims to rapidly expand the store network and is likely to increase expectations for the new business format. PPIH’s presence in the stock market is growing, as its shares were newly added to the Nikkei 225 during this spring’s periodic replacement. However, the stock price remains near the lower end of the trading range (JPY900–1,100) seen since last summer. Amid market conditions in which investors avoid international blue-chip stocks due to tensions in the Middle East, PPIH may be worth monitoring as a strong-performing, domestic-demand-related stock in Japan.

Discover datasets unique to the Japanese equity market

Visit QUICK Data Factory: https://corporate.quick.co.jp/data-factory/en/

Disclaimer:

https://corporate.quick.co.jp/en/terms/#disclaimer

Follow us on LinkedIn to stay updated with Japan Markets.